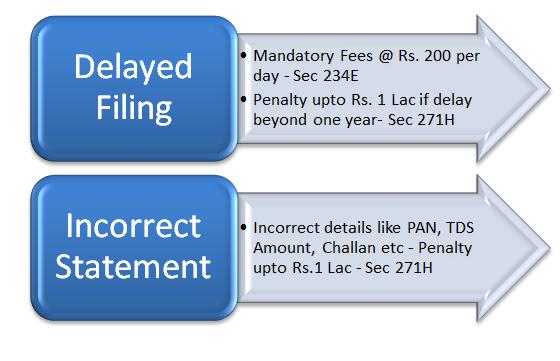

Almost all the Income Tax deductors are fed up with the penalties shooted up by the Income Tax Online Services Traces u/s 234E amounting Rs 200/- Per day or the Maximum of the amount of TDS which ever is lower.

Income Tax Department has amend the rule and implemented the section since 01-07-2012. All the TDS Return statements which are not filled under stipulated time frame are sent the notices with Penal Amount.

There are many offices which have received the penal amount limited to Two lacs and more.Deductor need to pay the penalty including the late fees with in the stipulated time.

Now the important Question, Whether the Late fees charged under 234E can be waived ?

It is heard that due to large number of default in filling TDS return statement, Income Tax may soften their stand and may waive the late fee for a specific period. But NOT GUARANTEED.

There are some legal constraint in Charging the Penalty Under Section 234E, i.e.

Section 234E states that :

[box type=”note” ]The amount of fee referred to in sub-section (1) shall be paid before delivering or causing to be delivered a statement in accordance with sub-section (3) of section 200 or the proviso to sub-section (3) of section 206C. [/box]

Statement clearly says that the late fees must be paid along with or before the submission of TDS return statement But income Tax accepted the Return statement without collecting the late fees and sent the penalty later which is not as per the rule of Income Tax u/s 234E.

Once the TDS return statement accepted by the Income Tax through any mean i.e. either Online or through facilitation center without late fees, the penalty can’t be recovered later as per the section 234E.

Section 200A clearly says that there is no provision for default in payment of late fee in Income Tax other than clerical mistake or Incorrect claim.

So, What I believe that Income Tax would change the rule first and give benefit of doubt ?