Highlights of the changes in the Income Tax New Policy, Rules by CBDT – checkout the new policy modification in Income Tax Rules for FY 2020-21. The major highlights of the new tax policy are:

Income Tax New disclosures asked in the new ITR forms 1 to 7 are:

1. House ownership: Individual taxpayers who are joint owners of house property cannot file ITR 1 or ITR4.

2. Passport: One needs to disclose the Passport number if held by the taxpayer. This is to be furnished both in ITR 1-Sahaj and ITR 4-Sugam. Hopefully, it will be made mandatory in other ITR Forms as and when they are notified.

3. Cash deposit: For those filing ITR 4-Sugam, it has been made compulsory to declare the amount deposited as cash in a bank account, if such amount exceeds Rs 1 crore during the FY.

4. Foreign travel: If you have spent more than Rs 2 lakh on travelling abroad during the FY, you need to disclose the actual amount spent.

5. Electricity consumption: If your electricity bills have been more than Rs 1 lakh in aggregate during the FY, you need to disclose the actual amount.

6. Investment details: Details of investment qualifying for deduction under chapter VIA with bifurcation of details of investment made during the period from April 1, 2020 to June 30, 2020.

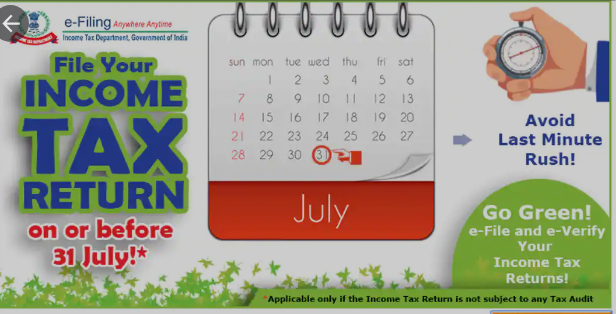

7. For every assessment year, the last date for filing tax returns is July 31, However, this year ITR filing date has been extended till November 30, 2020 due to pandemic Covid-19.

Also Read – New Changes in Form 26AS, Credit Cards & eWallets Added

8. Income Tax Exemptions and Deductions that you can claim under the New Tax Regime for FY 2020-21 (AY 2021-22): Withdrawal by an employee from the Employees’ Provident Fund (EPF) is not taxable after 5 years of continuous service.

9. Withdrawal from National Pension Scheme (NPS) on maturity or premature closure up to 40% of the amount received on such withdrawal remains tax free for all. In case of partial withdrawal from NPS, up to 25% of the contributions made by the individual will be tax free. Employer’s contribution to NPS up to 10% of their basic salary and dearness allowance also remains tax free.

10. Under Section 10 (10D) of the Income Tax Act, the sum assured and any bonus paid on maturity or surrender of the life insurance plan is tax free. Maturity proceeds continue to be exempt under Section 10(10D) even in the new regime. The maturity amount including interest received on the Sukanya Samriddhi Yojana will not attract any tax.

11. Conveyance Allowance granted to meet expenditure incurred on conveyance in performance of duties of an office and any allowance granted to an employee to meet the cost of travel on tour or on transfer (including relocation) are tax free.

Interest received from post office savings account balance up to ₹3,500 annually per individual will remain free from tax.

12. Any scholarship granted to meet education costs is tax exempt under Section 10 (16) of the Income Tax Act. Gratuity received from the employer up to ₹20 lakh after rendering 5 years of continuous service. Leave encashment received at the time of resignation or retirement up to ₹3 lakh.

13. Form 26AS will now be a complete profile of the taxpayer w.e.f. 01.06.2020, CBDT vide Notification dated May 28, 2020 amended Form 26AS in Sec 285BB w.e.f. 01.06.2020. Key takeaways are:

14. New form 26AS will also provide information in respect of “Specified financial transactions” which include transactions of purchase/ sale of goods, property, services, works contract, investment, expenditure, taking or accepting any loan or deposits of such value as may be prescribed but not less than of Rs 50,000.

15. Information about income tax demand, refund, proceedings pending, and proceedings completed which may include assessment, reassessment under section 148,153A 153C, revision, appeal will also be shared in this form 26AS.

16. Information on this form 26AS will not be a one-time affair at year end. This will be a live 26AS, as this will be updated regularly within 3 months from the end of the month in which such information is received.

Also Read – How to Check Fake Income Tax Return (ITR) For Loan ?

17. Form 26AS will now be a complete profile of the taxpayer for that particular year as against earlier form 26AS which just provided the information about taxes paid by way of TDS/TCS or self-assessing. This form will also have mobile no, email I’d and Aadhar no. of the taxpayer.

18. Further an enabling provision has been notified empowering the CBDT to authorise DG Systems or any other officer to upload in this form, information received from any other officer, authority under any law. Thus any adverse action initiated or taken or found or order passed under any other law such as custom , GST , Benami Law etc. including information about Turnover , import , export etc. will also be put in this form 26AS so that not only the concerned taxpayer but also all the Income Tax authorities will know and have access to such information.

19. This form 26AS will also provide information received by Tax Deptt from any other country under the treaty /exchange of information about income or assets of the taxpayer located outside India.

20. The implication of this new form 26AS will be that banks , financial institutions or any other authority or customer , buyer etc. while carrying out due diligence of the person/ corporate concerned will now ask for form 26AS so as to be sure that there are not any major issues about such person/corporates.